✅ Roughly speaking

📉 All Japanese car manufacturers in the Indonesian car market will fall below the previous year in 2025

🚗 China BYD gains 202.7% to gain 5.8% market share

⚡ 70% share of Japanese cars in front of crack

🔮 This happens across ASEAN 『a microcosm of the future』

✅ Audio summary of this post here

Introduction

This time, we will provide a detailed explanation of the dramatic structural changes that have occurred in the Indonesian automotive market in 2025, based on the latest data.

Indonesian Automobile Manufacturers Association (GAIKINDO: Gabungan Industri Kendaraan Bermotor Indonesia) The full-year 2025 statistics released by on January 13, 2026, were extremely tough for Japanese automakers.

As the overall market shrinks, the share of Japanese cars that have dominated the market for many years is rapidly declining, and Chinese EV brands are experiencing explosive growth.

Having myself been involved for many years in supporting business in the ASEAN region, I see this change as not just a business cycle, but a historic turning point in the automotive industry.

In this article, we will interpret the reality of this "tectonic shift" in numbers and consider the challenges facing Japanese companies and their future prospects.

a contraction of the overall market and 『an abnormal surge in imports』

2025 marks the second consecutive year of market contraction

The Indonesian automotive market in 2025 will clearly see a contraction, following on from the previous year. GAIKINDO Statistics According to the report, the key indicators are as follows:

| Indicator | 2024 results | 2025 results | Year on year |

|---|---|---|---|

| Wholesale sales volume | 865,723 units | 803,687 units | ▲7.2% |

| Retail sales | 889,680 units | 833,702 units | ▲6.3% |

| Number of units produced | 1,196,664 units | 1,147,600 units | ▲4.1% |

| Number of finished vehicle imports | 97,010 units | 176,593 units | +82.0% |

Macroeconomic factors such as rising interest rates, inflationary pressures and slowing economic growth are behind the market contraction.

However, what is noteworthy is that 82.0% increase in imports of finished vehicles This is an outlier.

What a surge in imports means

The fact that imports are up +82.0% while domestic production is down ▲4.1% clearly shows that the offensive for finished vehicles from overseas (mainly China) is in full swing.

This figure can be considered an important signal that the competitive environment in the Indonesian market is fundamentally changing.

JETRO Analysis As noted, the end of the tax incentive system for imported BEVs (battery electric vehicles) at the end of 2025 led to a rush to demand in December, with a single month hitting a record high of 94,100 units.

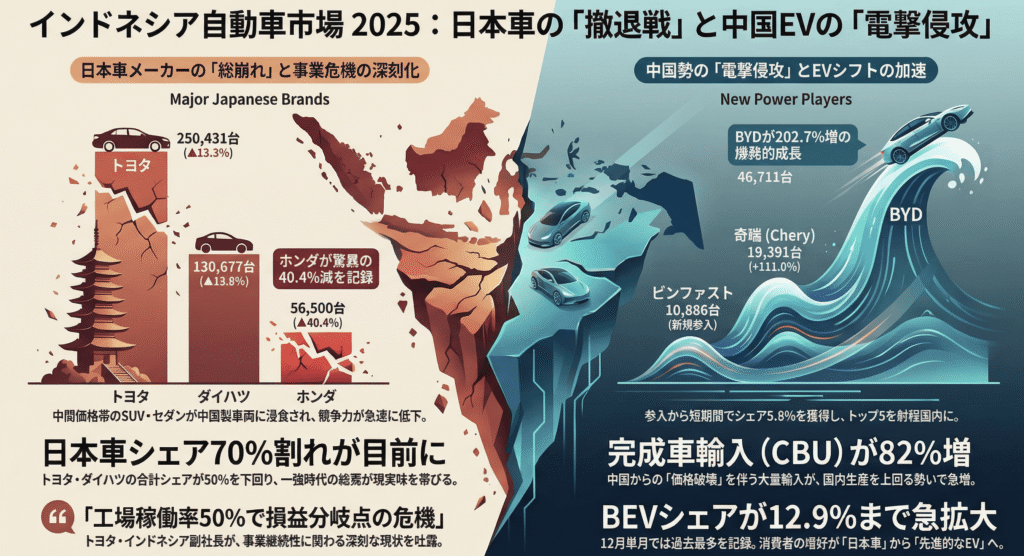

All five Japanese car manufacturers 『total collapse』── fell below the previous year

All five major brands struggle

2025 has been a nightmare for the Japanese car brand, which has long boasted a market share of over 90%.

GAIKINDO Statistics According to the report, all five major brands recorded a year-on-year decline.

| brand | Wholesale 2024 | Wholesale 2025 | Year on year | Share change |

|---|---|---|---|---|

| Toyota | 288,982 units | 250,431 units | ▲13.3% | 33.4% → 31.2% |

| Daihatsu | 163,032 units | 130,677 units | ▲19.8% | 18.8% → 16.3% |

| Honda | 94,742 units | 56,500 units | ▲40.4% | 10.9% → 7.0% |

| Mitsubishi Motors | 80,452 units | 71,781 units | ▲10.8% | 9.3% → 8.9% |

| Suzuki | 73,348 units | 66,345 units | ▲9.5% | 8.5% → 8.3% |

Honda's 40% decline indicates 『collapse in mid-price range』

Particularly serious is Honda's ▲40.4% drop.

The figures suggest a rapid loss of competitiveness in the market.

This highlights how Honda's specialty mid-range sedans and SUVs are being eroded by feature-packed, competitively priced Chinese-made vehicles.

The combined share of Toyota and Daihatsu also changes from their previous solid structure 47.5% 1999, and the lack of a majority is becoming the norm.

It is estimated that the overall share of Japanese cars has fallen to around 70%, and the end of the "era of the strongest Japanese cars" is becoming a reality.

Toyota Vice President's Crisis Statement

This situation is symbolized by Toyota Motor Corporation Indonesia Vice President Bob Adamu's remarks It is.

"We are currently at a critical level where factory utilization has fallen to about 50 percent and we are breaking even," he said.

This means that we have entered a phase where business continuity itself is being questioned, not just a decline in share.

The situation in which even a company as large as Toyota has to publicly acknowledge its woes in the Indonesian market can be considered a serious warning for the entire Japanese automotive industry.

Chinese 『Blitzkrieg』── BYD is already within the top five ranges

BYD's phenomenal growth

The group of EV brands, mainly Chinese, is taking over the market share of Japanese cars.

In particular BYD's growth has been phenomenal and has been within range of breaking into the top five within a short time of entering the market.

| brand | Wholesale 2024 | Wholesale 2025 | Year on year | share | Features |

|---|---|---|---|---|---|

| WORLD | 15,429 units | 46,711 units | +202.7% | 5.8% | EV specialist, importer |

| Chery (Chery) | 9,191 units | 19,391 units | +111.0% | 2.4% | China's major SUV strengthens |

| VinFast (VinFast) | ─ | 10,886 units | New | 1.4% | Vietnam EV, all quantities imported |

| DENZA (rising momentum) | ─ | 7,474 units | New | 0.9% | BYD luxury brand |

| AION | 1,240 units | 6,839 units | +451.5% | 0.9% | Guangzhou Automobile Series EV |

BYD alone Market share 5.8% I won.

The combined share of Chinese and emerging EV brands has reached around 15%, positioning them as "key players" rather than "niche players".

『Stock Offensive』 presents a Chinese-style market control strategy

It is noteworthy that the number of BYD imports far exceeds the number of wholesale units.

This portends a market offensive due to inventory buildup, and further price competition is expected to intensify in 2026.

The Chinese manufacturer has adopted the strategy of "first importing cheap finished vehicles to dominate the market and increase brand awareness, then moving to local production."

This method can also be considered a modern version of the strategy that once led Japanese manufacturers to succeed in the Southeast Asian market.

Three drivers of structural change

EV shifts and policy tailwinds

The Indonesian government's EV incentives (tax incentives and subsidies) are clearly working in favor of the Chinese.

Year-round sales by fuel Looking at it, the structural changes are clear.

| Fuel type | Number of units sold in 2025 | share |

|---|---|---|

| gasoline car | 455,948 units | 56.7% |

| BEV | 103,930 units | 12.9% |

| Diesel car | 173,240 units | 21.6% |

| TOGETHER | 65,323 units | 8.1% |

| PHEV | 5,235 units | 0.7% |

The share of BEVs 12.9% It reached a record high of 21,820 units in December alone.

Hybrids and internal combustion engine vehicles, which are the specialties of Japanese car manufacturers, are at a disadvantage both in terms of price and policy.

Realizing price destruction

An 82% increase in finished vehicle imports shows that Chinese manufacturers are seizing market share by using "price destruction" as a weapon.

Chinese-made EVs and SUVs are 20〜30% cheaper than Japanese cars with similar specifications, and come standard with more advanced features (such as large touch panels and autonomous driving assistance).

Consumer preferences are rapidly shifting from "reliable Japanese cars" to "advanced, affordable Chinese EVs."

This change is considered irreversible.

Expanding the used car market

Institute of Economic and Social Research, University of Indonesia (LPEM) According to the report, the new car market will remain at just over 800,000 units, while used car sales in 2024 will reach 1.8 million units.

The reality that consumers are shifting to the used car market due to rising new car prices and economic uncertainty is also putting pressure on new car sales among Japanese manufacturers.

2026 and beyond scenario ──choices left for Japanese car manufacturers

Pessimistic Scenario: BYD's Top 3

If current growth rates (+202%) continue, BYD will overtake Honda and Mitsubishi Motors in 2026 3rd in market share It is considered likely to emerge in.

The share of Japanese cars will fall to the 60% range, and the very premise of "Japanese car dominance" will collapse.

Realistic forecast: further market contraction and restructuring

"Effective stimulus measures to stimulate the industry are urgently needed," said Putu Juli Ardika, Chairman of GAIKINDO.

However, if government support measures do not work well enough, the market is expected to shrink by a further 5〜10% or so.

In this environment, some manufacturers may be forced to downsize their production lines or overhaul (including withdrawing) their Indonesian operations.

Remaining solutions for Japanese companies

The following measures are considered urgent for Japanese manufacturers to survive.

①Accelerating EV adoption

It may be too late, but we urgently need to expand our affordable BEV lineup.

We should hurry up and bring global models like Toyota's bZ4X and Honda's e:NY to Indonesia.

②A fundamental overhaul of pricing strategy

The "high quality, high price" strategy no longer works for the middle class.

We need to achieve a price range that can compete with Chinese forces by reducing costs and improving local procurement rates.

③Production optimization within ASEAN

It is important to review production sharing with Thailand and Vietnam and to seek economies of scale.

Optimization in Indonesia alone has limitations.

④or 『strategic withdrawal』

Unfortunately, not all manufacturers survive.

If market share is not expected to recover, an early decision to exit and redirect management resources to other markets may be an option.

This happens across ASEAN 『a microcosm of the future』

Indonesia is not a special case

This time, the changes in the Indonesian market are by no means a unique case.

Similar structural changes are underway in other major ASEAN markets, including Thailand, Vietnam and Malaysia.

Thailand :BYD will enter the top 10 in 2024, with the total share of Chinese brands exceeding 10%.

Vietnam :Local VinFast is dominating the EV market, and the share of Japanese cars is rapidly declining.

Malaysia :The government's policy to protect domestically produced vehicles and measures to promote EVs have undermined the dominance of Japanese vehicles.

From internal combustion engines to EVs, from Japan to China

This is not just a change in market share, From internal combustion engines to EVs , Japan to China It is a historical paradigm shift with a shift in initiative.

Japan's automotive industry faces the reality that the competitive advantages of "quality," "reliability," and "after-sales service" that it has cultivated over the past few decades will not function well under the rules of the new game of EVs.

summary

The 2025 Indonesian car market statistics marked a historic turning point, marking the end of the "era of the strongest Japanese car."

The figures of a 40% plunge in Honda, a 200% explosion in BYD and an 82% increase in imports of finished vehicles clearly show that this is no longer a temporary phenomenon but a structural tectonic shift.

For Japanese companies, a mere "protection" strategy is no longer enough.

There is an urgent need to accelerate EV deployment, reassess pricing strategies, and above all, adapt to "changed market needs."

In my own work supporting business in the ASEAN region, I have witnessed firsthand the struggles many Japanese companies face in responding to change.

But only companies that face this harsh reality and act quickly believe they can survive the next decade.

We expect 2026 to be a crucial moment for survival.

The changes taking place in the Indonesian market are a mirror that reflects the future not only of ASEAN but also of the global automotive industry.

comment